Despite China’s present technology boom, Internet penetration is still a mere 47%.

The recent news story about Bank of China allegedly assisting with illegal money transfer ended well for the bank and turned out to be a case of journalists not doing enough research...

Despite the regulators’ effort in boosting investor’s confidence in post-hiatus IPOs, growth in Chinese stock market growth in trading volume is still sluggish.

On June 11 2014, MSCI Inc. indicated that China’s A-shares will not be included in MSCI’s global index, meanwhile, South Korea and Taiwan will not be considered to upgrade to developed market status.

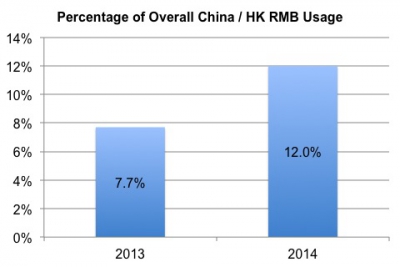

In the latest SWIFT RMB tracker report, usage of RMB in cross-border payments involving HK and China increased 36% to 12%, but still has ways to go.

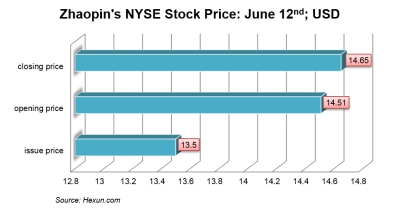

Shortly after Jumei Youpin, JD.com listed in US, Zhaopin, an online recruitment platform, listed on the NYSE on June 12th, 2014.

State Council is China’s main governing body and its opinions provide guidance for the financial industry and allow to peek into what the government has in mind for the markets in the coming years.

Since the IPO hiatus last year many qualified mainland companies have been waiting for new capital. With banks traditionally more supportive of SOEs and PE not being able to invest since much of their capital have been locked already, many well-managed, fast-growing companies were starving of capital.

The RMB continued its relentless march towards being a trade currency with over US$15 billion in RMB bond issuance in the city-state of Singapore - more than doubling the issuance of 10 years ago.

On May 22nd, JD.com listed on NASDAQ, with the timing being somewhat of a surprise for many market observers.

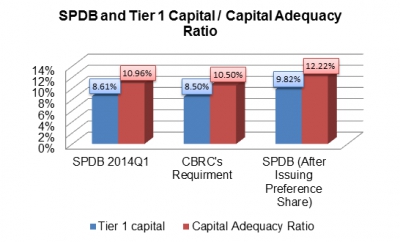

With the introduction of regulations on preference shares by the CBRC and PBOC in this March and April, banks seem to be willing to explore the new financing option.

According to the latest numbers from Ministry of Commerce of PRC, in the first 4 months of 2014, the investment into Hong Kong from Mainland and exports from Chinese mainland to Hong Kong decreased largely.

The latest figure announced by the CSRC indicates that in early 2014, the number of Chinese securities investment funds registered increased, with the total turnover declined dramatically.

In year 2014 we expect to see numerous new policy and regulation updates on the financial reform of Shanghai FTZ. Where are we today?

Shanghai local government and Chinese central government will endeavor to expand the market functions, deepen the opening of local financial markets to foreign investors, increase the number of financial institutions in the FTZ, encourage the financial business innovation and make Shanghai more of an international financial center.

Some of China's financial reforms are under consideration or have already been executed in 2014, such as setting up crude oil futures, international gold trading, financial asset trading, syndicated loan trading platforms and building nationwide trust registry service institutions. Besides, rules regarding foreign and FTZ-registered firms’ parent companies RMB bonds issuance are on the way. Moreover, Shanghai FTZ regulators will also consider introduction of free trade account management by allowing financial institutions to set up FTA (Free Trade Account) accounting units segregated for residents and non-residents. Furthermore, Shanghai FTZ regulators encourage direct investment abroad from local firms and private equity funds. The main contents of Shanghai FTZ’s reform could be described as a ‘1+4’ policy, where ‘1’ stands for risk control segregate account system; ‘4’ stands for interest rate liberalization, foreign exchange liberalization, RMB cross-border utilization and RMB capital account opening.

FX reform and FTA accounts

PBOC announced that, starting on March 17, 2014, the interbank RMB/USD spot price’s fluctuation spread increased from 1% to 2%. For commercial banks, the fluctuation range of RMB/USD spot price offering to the clients could be expanded from 2% to 3% from the mid-price calculated by Chinese interbank FX market. This is the third time for PBOC to expand the fluctuation range. Analysts say the expansion in RMB/USD spot fluctuation range is a clear signal that RMB will be internationalized in the near future and Shanghai FTZ is thought to be a test-bed for that. The most prominent aspect of Shanghai FTZ FX reform is the FTA (Free Trade Account). FTA is essentially a free trade bank account for Shanghai FTZ registered firms, very similar to an offshore bank account, which enables free capital flow inside the FTZ. FTA system allows both foreigners and local residents to get their money in and out through FTZ. Overall, there are mainly 3 types of FTA accounts. Local firms in the FTZ could open FTA accounts; individuals in the FTZ could open FTA accounts; foreign firms in the FTZ could open FTN accounts. As regulators are treading conservatively with hot money inflows and money laundering risks in mind, there is still no detailed timeline. However, we believe the FTA mechanism will be released in 2014 or 2015 as a momentous milestone in China's financial reform history.

Interest rate reform

In March, 2014, a PBOC official claimed that the sequence of Shanghai FTZ interest rate reform will be ‘liberalize interest rates for foreign currencies prior to RMB interest rates; free the loan rates prior the deposit rates’.

There were actions towards interest rate reform in Shanghai FTZ from the regulators. PBOC announced that from March 1st, 2014, the deposit rate of foreign currencies below the amount of USD3 million would be liberalized, which actually removed the ceiling for foreign currencies’ deposit rate. This is thought to be an important step on the road to fully liberalized interest rate reform. The next step could be liberalization of the deposit rates of the local currency, which may not only be applicable in Shanghai FTZ, but also the rest of China.

Cross-border RMB utilization

On Feb 21, 2014, PBOC released the detailed regulation on expanding the usage of RMB overseas, which simplified the process of RMB overseas usage under current and direct investment account. However, overseas RMB financial scale and usage range will still be restricted, as well as cross-border e-commerce transactions and RMB trading services.

Six banks constitute the first batch of firms applied for the cross-border RMB settlement licenses. ICBC and Bank of China helped their clients within the zone to make an overseas RMB loan; Bank of Shanghai, HSBC and Citi Bank launched cross-border RMB current account centralized collection and payment services; Bank of Communications signed the first overseas RMB borrowing service for the non-bank financial institutions.

Capital account liberalization (to be announced)

In the future, the capital account might be opened for local and foreign investors. As Chinese reformers are relatively prudent and conservative, the liberalization process of capital accounts have been advancing relatively slowly so far. One important step in the process will be a gradual opening of commercial futures market to foreign institutional investors.

2014 version of ‘negative list’ (possibly to be released in the 1st half of 2014)

In the 1st half of 2014, a new version of ‘negative list’ will be released to update the 2013 version. Although it is not clear what items this version may include, there are two aspects which are certain. One aspect is that the contents included in the negative item list will be shortened, which implies that the restrictions on types of companies to register in the zone will be reduced. The other aspect is that Shanghai FTZ might cooperate with Hong Kong to introduce advanced practices from the city.

We also have an in-depth report on Shanghai FTZ available here.

Cracks are starting to show in the once impervious armor of China's online finance platforms as yields have dropped 20% from their highs. Ranging from about 4.7-5.6%, the current highs are much lower than the 6-8% that we saw at the end of 2013 and beginning of 2014.

China's online finance platforms facing headwinds

Realistically though, this isn't surprising. As we have discussed before, these platforms were running on borrowed time. Whilst the business model made sense, the inter-bank lending rates and the negotiated deposits that the main China online finance platforms were able to negotiate were a bit of a perfect storm for the platforms.

Now as the banks have put limits in place on the amount of money that can be moved on and off the platform at any one time, we're starting to see the market's reaction to what has caught most banks and the regulators completely off-guard. This is unlikely to be the last push-back from the banks on these new financial products.

Unclear Regulation

Yet the platforms still have over 1.45 trillion yuan (US$230+ billion) on their platforms and this is unlikely to rapidly decrease anytime soon. 4-5% is still much better than the average retail consumer could get on a bank demand deposit in most of China's main banks and the convenience can't be beat - very easy to get money on and off the platforms, although within the limits set out by the PBOC.

This is far from the end of the story thought. We expect the growth of the platforms to certainly slow and although its still a bit unclear as to what the regulation will be, further regulation and requirements from the PBOC is inevitable as we go forward in 2014. This is all the more critical as Alibaba moves forward on the IPO plans. Can the company count on that part of the business to still drive revenue?

The latest figures from online saving funds financial statements have shown that the BAT (Baidu, Alibaba, Tencent) online money funds continued expanding. The 2014Q1 data reveals that Tianghong Zenglibao, relying on the huge client base of Yuebao, lead the market and is the first online saving funds that exceeds RMB100 Billion.

On April 10, 2014, the Chinese government approved the proposal for Hong Kong-Shanghai Stock Market Connect program, which will allow mainland investors to directly trade stocks in Hong Kong market and Hong Kong investors to trade equities in A-share markets.

Over the next week, we'll be publishing a number of articles looking at the upcoming Alibaba IPO which could be the largest tech IPO ever. Today we look at the financials filed with the SEC.

On April 14, 2014, Shanghai Stock Exchange-traded *ST Changyou was delisted, becoming the first state owned company to be delisted in A-share markets.

As US SEC’s investigation on large investment banks recruiting Chinese governmental officials’ and SOE senior managers’ children is going further than any such probe before, the dark side of foreign companies operating in Chinese markets is gradually being exposed to the public. However, that probably doesn’t come as a surprise for the Chinese public which has known and suffered from the ‘unwritten rules’ for a long time.

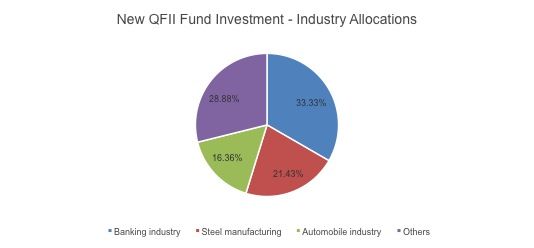

The latest statistics about the A-share markets illustrate the main industries that QFII funds invested at the end of 2013, according to data from 1334 listed firms’ 2013 annual reports. The banking industry is the most attractive industry for QFII investors, taking about 1/3 of the total new shareholding volume with the steel industry and automobile industry ranked the 2nd and the 3rd.

The banking industry makes sense because of the relatively low valuations. The steel industry is currently suffering in China, so QFIIs likely have confidence that Chinese urbanization and development of automobile industry will continue. For automobile industry, as Chinese government intends to push hardly on new energy vehicles especially electricity-powered vehicles, could pose an interesting QFII investment allocaction.

High frequency trading (HFT) has roughly been in existence since 1999 in the US as execution times have shortened from several seconds to millisecond or even microseconds due to advanced trading technologies and a general demand for increased speed. Figures from August 2013 showed that in the global FX market, HFT took approximately 40% of the total trading volume, within which, almost half of the volume happened in the spot market. For the global futures market, HFT volume represents about 40% of the total volume. In the equities market in the US, HFT volume took approximately 73% of all equity order volume. Typical strategies executed by HFT traders are trading ahead of index fund rebalancing, market making, ticker tape trading, event arbitrage, statistical arbitrage, news-based trading and low-latency strategies.

You'd be forgiven for missing it, but in the buying spree that we've seen in the last couple of weeks from Alibaba, one of the most significant investments was for a controlling stake in Hundsun Technologies. The ~US$532M investment in the firm means that Alibaba now has control of nearly 95% of all domestic trading systems in China and continues to consolidate its position as a financial technology provider.

A couple of days ago, media announced that Alibaba had made a substantial investment in InTime, which is a Hong Kong company that manages mainland China upper-end retail malls. These malls are typically branded InTime, but are multi-brand inside where each brand has a small section and potentially dedicated staff to that section.

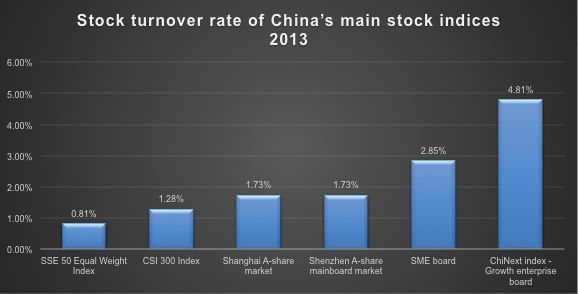

On March 3, 2014, the chairman of the council of the Shanghai stock exchange Gui Minjie declared that there is no technical barrier for the release of T+0 trading mechanism specially for blue-chip stocks traded on Shanghai Stock Exchange. The chart below showed that the large-cap stocks based indices have lower turnover rate than the indices with more proportion of small and mid-cap stocks. The T+0 in Shanghai Stock Exchange could possibly stimulate the trading of large-cap stocks on A-share markets. The speech of Mr. Gui implied that the T+0 mechanism might be close to launch in 2014.

February 2014, represented another month of decreasing commission fees in China's capital markets as the entrance of China's technology giants in internet finance starts to affect not just banks, who are losing deposits, but securities brokers whose fees are being squeezed.

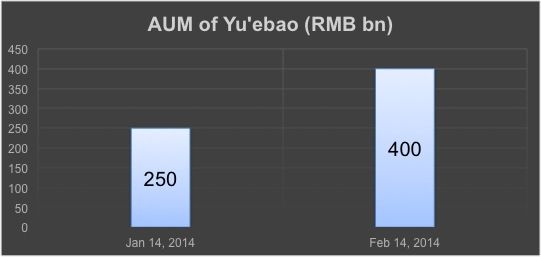

Yu’ebao had already made Tianhong Asset Management the largest one in the public fund industry in China in early 2014. However, the scale of Yu’ebao has continued to grow with the latest figures showing the AUM of Yu’ebao reaching RMB400bn on Feb 14, 2014, a leap of 60% compared to only one month ago. The speed of capital inflow is still accelerating in 2014. We may witness Yu'ebao becoming the largest money market fund in the world soon.

The fast expansion of  Yue bao AUM data of Chinese money market funds, especially the ones leveraging Internet Finance, reflects the large wealth management demand potential of Chinese market and new innovative finance forms that will appear in the Chinese market in 2014.

Yue bao AUM data of Chinese money market funds, especially the ones leveraging Internet Finance, reflects the large wealth management demand potential of Chinese market and new innovative finance forms that will appear in the Chinese market in 2014.

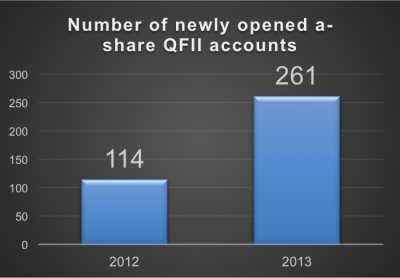

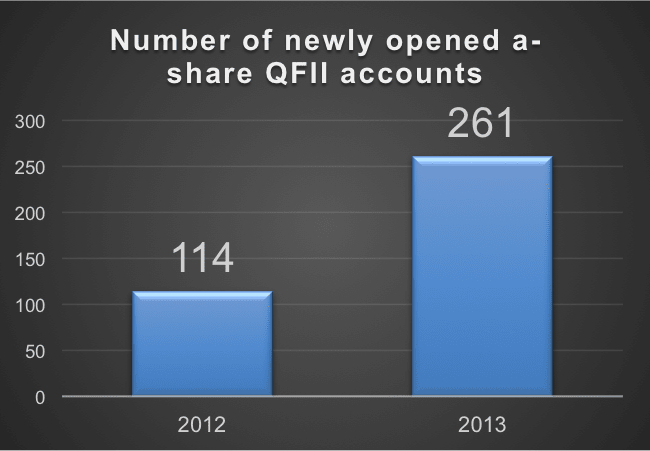

According to data from the China Securities Depository and Clearing Corporation Limited (CSDC), there were 261 new Qualified Foreign Institutional Investor (QFII) accounts opened in 2013 which represents about 43% of the total QFII account number from 2003 to 2013. Compared to 2012 figure. Number of QFII accounts rises by 129%.

So why are foreign investment institutions so interested in opening up accounts to trade the Chinese market when returns are so low? One reason is that the mainland regulators have been pushing towards more open markets and lowering the QFII requirements with the intent of introducing foreign capital to provide better liquidity in an anemic a-share mainland market. In addition to new accounts, more than $49.7 billion in QFII investment quota was approved in 2013.

The potential second reason is that foreign investors see potential opportunities in the mainland market either with current relatively low valuations or in the anticipation of future market growth if the market does pick up.

The Shanghai Stock Exchange has been in the doldrums for the past couple of years and was the worst performing Asian exchange of 2013.

2013 will remembered as an incredibly dynamic year for China’s financial services industry. From the increasing number of hedge funds in the market to the emergence and regulation of Bitcoin, industry observers, investors, participants and regulators have had their work cut out for them keeping up with the market.

More...

On November 27, 2013, the Ali-cloud division of Alibaba group announced the launch of Ali Financial Cloud services.

Background

Ali financial cloud services has been developed to provide secure and stable IT resources and internet operation services for financial institutions including banks, funds, insurance companies and securities companies. The service is based on cloud computing, with the cooperation from many well-known financial product solution providers and Alipay’s standard connection portal and a completely sandboxed environment.

At current stage, China's approximately 2,000 small and medium banks are the focus of Ali Financial Cloud as these banks typically do not have enough capital and technology experience to develop their own robust IT structure, so outsourcing is thought to be a low cost and efficient way for these banks to process large amount of data and information.

The claimed benefits Ali Financial Cloud include:

- Enable Small and medium banks to have their own online banking system and mobile banking systems and expand e-commerce and online banking services in the rural areas.

- Provide stable and strong business processing capabilities for small and medium banks during high demand periods

- Enable small and medium banks with smaller technology footprints to develop innovative products and solutions that would typically only be available to larger banks

- Reduce IT support requirements

One example provided by Ali cloud website shows the processing capabilities of Ali cloud. About 300 million transactions of Yu’ebao could be cleared within 140 minutes, or about 35,000 transactions per second. Some financial firms are already using the Ali fianancial cloud including asset management companies, rural banks, regional banks and insurance companies.

Historical Context

Cloud computing in China's financial services industry, similar to other global markets, has been slow to take off. Players like IBM have in the past setup comprehensive cloud computing research centers to attempt to move the market, but none have been incredibly successful in gaining a foothold.

2014 might be the year when we see this change. Cloud technology and security has become increasingly sophisticated and with an increasing profit squeeze due to liberalising interest rates, banks will be looking for ways to increase revenue, reduce cost, and more importantly, stay innovative.

2014 - Year of the Cloud

Certainly Cloud will be a key industry topic as we move into 2014 with major players besides Alibaba including IBM, 21Vianet and Tencent all vying for a part of the increasing cloud computing pie.

It will also be interesting to see the level of innovation that happens in the space. Alibaba has rapidly moved beyond just an IT / e-commerce company to provide a variety of products and services beyond just technology. Its Yu-ebao product is forcing banks to re-think their retail investment products and how they price and distribute them – it has completely changed the industry.

With China's cloud services in the financial indusry being a key topic of discussion in 2014, could we see Alibaba do the same thing it has with 3rd Party Payment Platforms?

The China Securities Regulatory Committee (CSRC) announced in December that the currently non-active A-share IPO market would reopen at the end of January, 2014.

Shanghai Stock Exchange and China Securities Index co.ltd announced that the new TMT (Technology, Media and Telecom) industry index and national defense indices would be released on December 25th, 2013.

Hongkou is a geographic district in Shanghai, on the west side of the Huangpu River, north of the center of Shanghai and close to Pudong District. The Hongkou Hedge Fund Park was officially established on Oct. 18, 2013, as the first test-bed specifically for developing local hedge fund industry and introducing foreign hedge funds in China. Through market reforms and special incentives, the Hongkou government hopes to make the Hedge Fund Park a key part of Shanghai, and indeed China’s, hedge fund industry.