Latest Insight

- Why cash is still prevalent in Asia

- Japan steps up green finance efforts

- South Korea charts middle path on crypto

- Should Grab and GoTo merge?

- Singapore pushes ahead with fintech-driven sustainability

- Digital banks in South Korea continue to thrive

- Billease is the rare profitable BNPL firm

- Fintech sector in Pakistan faces mounting challenges

- Where digital banks in Asia can make a difference

- Cashless payments jump in Vietnam

Latest Reports

-

Breaking Borders

Despite progress in payment systems, the absence of a unified, cross-border Real-Time Payments (RTP) network means that intermediaries play a crucial role in facilitating connectivity. This report examines the ongoing complexities, challenges, and initiatives in creating a seamless payment landscape across Asia. Innovate to Elevate

Despite progress in payment systems, the absence of a unified, cross-border Real-Time Payments (RTP) network means that intermediaries play a crucial role in facilitating connectivity. This report examines the ongoing complexities, challenges, and initiatives in creating a seamless payment landscape across Asia. Innovate to Elevate In the dynamic and diverse financial landscape of the Asia-Pacific (APAC) region, banks are at a pivotal juncture, facing the twin imperatives of innovation and resilience to meet evolving consumer expectations and navigate digital disruption. Catalyzing Wealth Management In The Modern Era

In the dynamic and diverse financial landscape of the Asia-Pacific (APAC) region, banks are at a pivotal juncture, facing the twin imperatives of innovation and resilience to meet evolving consumer expectations and navigate digital disruption. Catalyzing Wealth Management In The Modern Era Hyper-personalized wealth management presents a paradigm shift from traditional models relying on static, generalized segments. Developing tailored investor personas based on psychographics, behaviours and fluid financial goals enables financial institutions to deliver rich and tailored customer experiences that resonate with next-generation priorities.

Hyper-personalized wealth management presents a paradigm shift from traditional models relying on static, generalized segments. Developing tailored investor personas based on psychographics, behaviours and fluid financial goals enables financial institutions to deliver rich and tailored customer experiences that resonate with next-generation priorities.

Events

| April 23, 2024 - April 25, 2024 Money 2020 Asia 2024 |

| October 21, 2024 - October 24, 2024 Sibos Beijing |

| November 06, 2024 - November 08, 2024 Singapore Fintech Festival |

2013 will remembered as an incredibly dynamic year for China’s financial services industry. From the increasing number of hedge funds in the market to the emergence and regulation of Bitcoin, industry observers, investors, participants and regulators have had their work cut out for them keeping up with the market.

Over the past week, Robocoin Technologies announced they were expanding their Bitcoin ATM offering into Asia with planned ATM installs in Taiwan and Hong Kong.

On November 27, 2013, the Ali-cloud division of Alibaba group announced the launch of Ali Financial Cloud services.

Background

Ali financial cloud services has been developed to provide secure and stable IT resources and internet operation services for financial institutions including banks, funds, insurance companies and securities companies. The service is based on cloud computing, with the cooperation from many well-known financial product solution providers and Alipay’s standard connection portal and a completely sandboxed environment.

At current stage, China's approximately 2,000 small and medium banks are the focus of Ali Financial Cloud as these banks typically do not have enough capital and technology experience to develop their own robust IT structure, so outsourcing is thought to be a low cost and efficient way for these banks to process large amount of data and information.

The claimed benefits Ali Financial Cloud include:

- Enable Small and medium banks to have their own online banking system and mobile banking systems and expand e-commerce and online banking services in the rural areas.

- Provide stable and strong business processing capabilities for small and medium banks during high demand periods

- Enable small and medium banks with smaller technology footprints to develop innovative products and solutions that would typically only be available to larger banks

- Reduce IT support requirements

One example provided by Ali cloud website shows the processing capabilities of Ali cloud. About 300 million transactions of Yu’ebao could be cleared within 140 minutes, or about 35,000 transactions per second. Some financial firms are already using the Ali fianancial cloud including asset management companies, rural banks, regional banks and insurance companies.

Historical Context

Cloud computing in China's financial services industry, similar to other global markets, has been slow to take off. Players like IBM have in the past setup comprehensive cloud computing research centers to attempt to move the market, but none have been incredibly successful in gaining a foothold.

2014 might be the year when we see this change. Cloud technology and security has become increasingly sophisticated and with an increasing profit squeeze due to liberalising interest rates, banks will be looking for ways to increase revenue, reduce cost, and more importantly, stay innovative.

2014 - Year of the Cloud

Certainly Cloud will be a key industry topic as we move into 2014 with major players besides Alibaba including IBM, 21Vianet and Tencent all vying for a part of the increasing cloud computing pie.

It will also be interesting to see the level of innovation that happens in the space. Alibaba has rapidly moved beyond just an IT / e-commerce company to provide a variety of products and services beyond just technology. Its Yu-ebao product is forcing banks to re-think their retail investment products and how they price and distribute them – it has completely changed the industry.

With China's cloud services in the financial indusry being a key topic of discussion in 2014, could we see Alibaba do the same thing it has with 3rd Party Payment Platforms?

The China Securities Regulatory Committee (CSRC) announced in December that the currently non-active A-share IPO market would reopen at the end of January, 2014.

It sounds trite if you’ve read my other posts on Bitcoin in China, but ‘wow! What a week it has been for Bitcoin in China’. With the PBOC effectively cutting off (legal) funding of accounts on exchange platforms, is there a future for the currency in China?

Shanghai Stock Exchange and China Securities Index co.ltd announced that the new TMT (Technology, Media and Telecom) industry index and national defense indices would be released on December 25th, 2013.

Kapronasia began researching Bitcoin in China in August 2013. Our Bitcoin in China report released on September 18th mentioned that in the future there would be two factors that really influence the fate of Bitcoin in China: the Chinese government’s attitude towards Bitcoin and Bitcoin’s acceptance as a method of payment, at least initially, by merchants.

2013 will remembered as an incredibly dynamic year for China’s financial services industry. From the increasing number of hedge funds in the market to the emergence and regulation of Bitcoin, industry observers, investors, participants and regulators have had their work cut out for them keeping up with the market.

The year started out with the prospects of a new government taking a new stance on reforming what had been a highly regulated financial services industry; we weren’t disappointed. Regulators unveiled a reform agenda both at the fall plenary session and throughout the year that has, and will have, a significant impact on interest rate reform, capital market investment in and out of China and the financial industry as a whole. Although some of the measures are still somewhat vague, some of the implementations, including the removal of the floor on lending rates, have already have a significant impact on banking profitability – it will be a new market in 2014.

China's finance in 2013 also brought an increased focus on development zones and centers. Opened to much fanfare, but little detail, the Shanghai Pilot Free Trade Zone (FTZ) was formally established in late September. Although it is still early days, if news reports and indications from the regulators are to be believed, the FTZ promises to be a new test-bed of reform for ‘value-add’ services similar to what Shenzhen was to the manufacturing / production industry in the late 70s and early 80s; arguably, one of the most important developments in China’s economic history. Smaller initiatives such as the Hongkou Hedge Fund Center in Shanghai sought to make it easier for hedge funds to enter the market and trade on China’s expanding base of capital markets products.

And last but certainly not least, we would be remiss if we didn't touch on Bitcoin. Chinese investors and tech enthusiasts were truly ‘chomping at the bit’ in 2013 as Bitcoin went from a little known US$13 cryptocurrency, to a US$1,000 potential economic destabilizer. China topped the world in Bitcoin wallets in May 2013 and then surpassed that again in November with over 150,000 wallet downloads. With the world’s biggest Bitcoin exchange and increasing popularity, China had little choice but to weigh in on the matter and in early December the People’s Bank of China annouced that Bitcoin was not a currency, banks could not deal in it, yet it could continue to be used in China. The price of Bitcoin fell, only to rise almost immediately afterward.

Will the sequel to 2013 in 2014 be as exciting? Will Xi Jinping continue to push reforms? Can the PBOC accept Bitcoins as a legitimate currency? Whatever happens, 2014 will be another dynamic year for Chinese markets and we’ll be here every step of the way to help you understand what’s happening in China’s financial services industry.

After 18 years of economic development, China’s Tier 2 Banks, mainly city commercial banks, are growing to fill a gap in-between state-owned banks, and rural commercial banks. As part of their growth, many city commercial banks are attempting to expand their branches in other regions, however, the Chinese Banking Regulatory Committee (CBRC) regulations are, in certain cases, holding them back.

The recent tight regulation regarding supra-regional city commercial banks is largely the result of increasing internal fraud cases in city commercial banks such as Qilu Bank and Hankou Bank. The good news is that the CBRC is not prohibiting city commercial banks from expanding supra-regionally. Instead, the approval process is just longer and the standard of regulatory evaluation indicators such as asset scale, capital adequacy ratio, profit margin, and non-performing loan ratios are higher than before. In this case, if city commercial banks attempt to expand outlets in other regions, they need to enhance their internal control and risk management abilities above the required standard.

Because the asset scale and business model vary based on the local economies in each city, the evaluation regulation will be different. If the investment in other regions is excessive, the CBRC will require a higher capital adequacy ratio; if the risk management does not match the fast growing asset scale, the CBRC will restrict the expansion of these city commercial banks. Thus, regulators support supra-regional expansion if the tier 2 banks meet the entire set of regulatory requirements.

China’s tier two banks are some of the more dynamic banks in China in terms of business models and innovation – they have had to be in order to compete with their larger counterparts that typically have much larger deposit bases and distribution networks.

The tier-2 banks are still focused on expanding their asset base and while supra-regional expansion will help them accomplish this, it is not the ultimate goal of the banks, at least not in the near future. The regulations do serve a valuable purpose to ensure that banks’ expansion is based on quality assets and business practices.

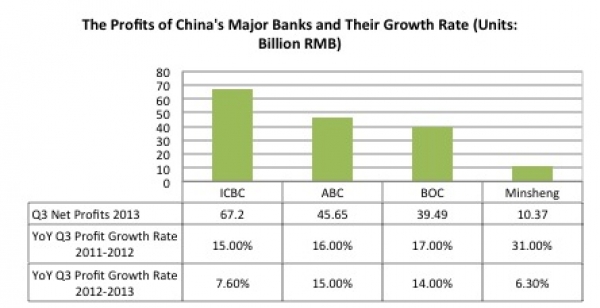

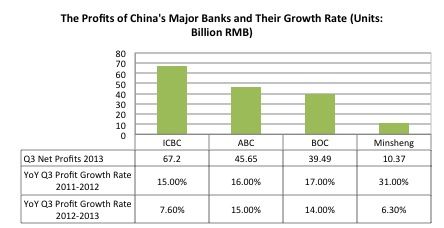

As fixed interest rates in China start to loosen up, banks' bottom lines are starting to feel the pressure. According to the latest figures from China major banks’ annual reports, the net profits of China Mingsheng Banking Corp.(Minsheng), Industrial & Commercial Bank of China Ltd.,(ICBC), Bank of China Ltd. (BOC) and Agricultural Bank of China (ABC) in the third quarter 2013 shrank on a YOY base.

As shown in the graph below, the net profits growth rate of Minsheng, a relatively smaller bank, dropped dramatically almost 25% comparing with the same period last year, likely due to its relatively large interbank business, which was heavily affected by high interest rates in the middle of June. The high interest rates in China also had a big impact on ICBC. The banks' profitability growth rate dropped to around 7.5%.

More...

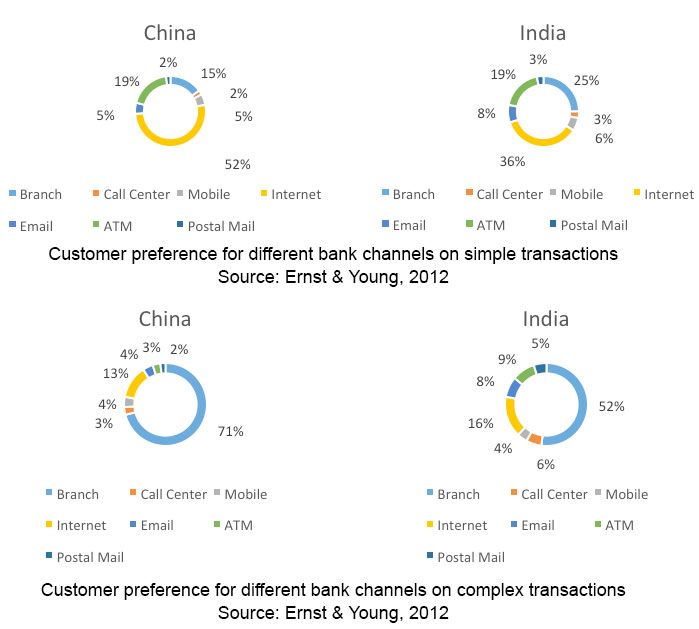

With a wide range of channel choices for retail customers, banks need to be aware of the usage and preferences for each channel which can vary for multiple reasons including the purpose of the transaction, complexity and where the person is from.

On the digital channel, customers usually require a fast and convenient service such as simple transaction or checking an account balance, but for branch service, customers, especially affluent customers require tailored personal interactions such as loan servicing, investment advice, and other complex transactions.

In self-service channels, Asian customers not only need a convenient and easy channel, but also a personalized interactive service to increase their loyalty to the bank as competition is rising and switching costs are lowering, especially in the wealth management space.

These wealthier customers produce higher value for banks, and usually they have a wide range of choices on banking services. In Asia, affluent customers show greater loyalty to their banks, while in most European countries and the U.S., affluent customers have relatively lower loyalty to their banks. Thus, maintaining affluent customers is important for banks to generate higher revenues.

Citi, one of the major players in Asia's wealth management space offers tailored services in Singapore. Their Citigold service provides a dedicated center for nonresident Indians. The personalized interaction improved the loyalty from their affluent customers because Citigold satisfied nonresident Indians’ special requirement on banking services.

However, China is showing a significant gap between affluent and mass-market customers on loyalty because the affluent customers receive much better service from their bank than mass-market customers do.

Banks should not only rely on channel innovation but also focus on improving service on the existing channels. Maintaining the existing affluent customers with tailored service is crucial to the bank since the affluent customers will continually show a high loyalty to their banks in Asia, but enhancing a required service or product for mass-market customers through different bank channels will also increase the overall customer loyalty.

Hongkou is a geographic district in Shanghai, on the west side of the Huangpu River, north of the center of Shanghai and close to Pudong District. The Hongkou Hedge Fund Park was officially established on Oct. 18, 2013, as the first test-bed specifically for developing local hedge fund industry and introducing foreign hedge funds in China. Through market reforms and special incentives, the Hongkou government hopes to make the Hedge Fund Park a key part of Shanghai, and indeed China’s, hedge fund industry.

The latest figures from Tianhong Asset Management show that the AUM (asset under management) of Yu’ebao deposits, the currency market fund which is co-launched by Alibaba and Tianhong on 13 June, 2013, has rocketed from June 13th to November 14th, 2013, from 0 to CNY100B. Now Yu’ebao is the largest fund in China leveraging it's enormous Taobao, T-mall and Alipay customer base.

The latest figures from Tianhong Asset Management show that the AUM (asset under management) of Yu’ebao deposits, the currency market fund which is co-launched by Alibaba and Tianhong on 13 June, 2013, has rocketed from June 13th to November 14th, 2013, from 0 to CNY100B. Now Yu’ebao is the largest fund in China leveraging it's enormous Taobao, T-mall and Alipay customer base.

The success story of Yu’ebao has not only encouraged the Chinese IT giants and online payment providers to enter the asset management market, but also is a worry to the traditional asset management firms. Currently, most public funds in China sell their products on their own websites or choose to cooperate with the online platforms to sell their products. Asset managers do recognise the benefit of selling funds online including low cost and convenience, but struggle as they simply just do not have the customer base of Alibaba/Alipay.

| Date | 13 June | 30 June | 9 Sept | 14 Nov |

| AUM (CNYB) | 0 | 6.6 | 55.65 | 100 |

From purchasing property with Bitcoins, to the world’s largest Bitcoin exchange, to incredible mining operations, China over the past few months has become the largest Bitcoin market in the world and a key part of the Bitcoin story.

To a large extent, Asian banks are in a somewhat enviable position. China is certainly the economic giant of the region, and if China’s economy slows, it does have knock-on effects, yet, the economies of individual countries in Asia, while interdependent, often expand and contract quite independently. This can mean a bank facing slower growth in Indonesia, might look to the Philippines or Malaysia for expansion.