China Banking Research

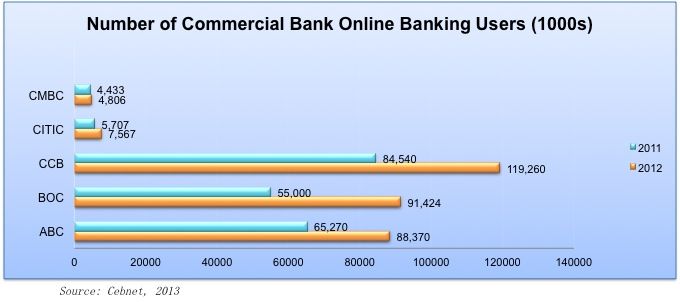

As the end of 2012, the total number of Chinese online banking registered users reached about 489 million. More specifically, according to the data released from Cebnet, CCB’s online banking customers increased to 119.26 million, jumping by 41% from 2011 to 2012. The number of BOC’s online banking customers has reached to 91.42 million, with a year-on-year growth rate of 66%.

Because of the dramatic increase in the number of online banking users, banks such as ICBC and CCB have launched more innovative personal banking services such as social insurance and wealth management services.

According to the CBRC, China’s commercial banks announced a total net profit of 1.24 trillion RMB in 2012, with the total net profit of the 16 listed banks comprising 1.03 trillion of that total. Among these 16 listed banks, the five major banks ICBC, ABC, BOC, CCB, and BOCom earned 239, 145, 139, 194, and 58 billion RMB respectively in 2012. China Merchants Bank (CMB) made 45.3 billion RMB net profit in 2012, topping other joint-stock banks. Bank of Beijing, as the leading city commercial bank in China, earned 11.7 billion RMB net profit last year. However, the overall net profit growth rate of China’s commercial banks has declined compared to 2011 apparently due to the process of interest marketization which has deceased interest based revenue recently.

NPLs in Chinese Banks Trending upwards again

According to the China Securities Journal, the quality of credit assets is again appearing as an issue for Chinese banks. The latest annual report shows that the non-performing loan (NPL) balance and non-performing loan (NPL) ratio both increased in 2012, a sharp move from the “double decreasing” in both NPL balance and NPL ratio in the previous years.

According to the China Securities Journal, the quality of credit assets is again appearing as an issue for Chinese banks. The latest annual report shows that the non-performing loan (NPL) balance and non-performing loan (NPL) ratio both increased in 2012, a sharp move from the “double decreasing” in both NPL balance and NPL ratio in the previous years.

The total NPL balance in the 11 listed banks was ¥385.38 billion in 2012 with a YOY growth rate of 8.1% compared to ¥356.6 billion in 2011. China Construction Bank believes the upward trend in NPL is due to the macroeconomic fluctuations in manufacturing, wholesale and retail trade, and real estate.

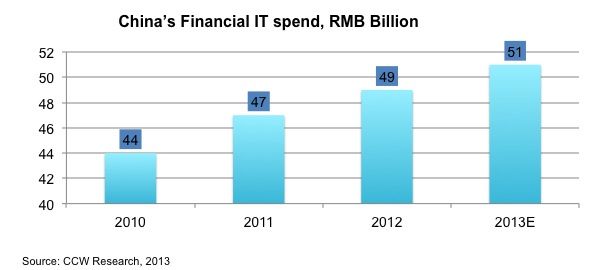

According to CCW Research, a local Chinese IT market research company, China’s financial industry IT software spend in 2012 grew to 49 billion RMB and the spending will keep a steady growth in 2013. Banking segment spend is a key driver, making up about 72% of total spend. Comprehensive risk management and big data are the main IT focus areas for banks.

As securities companies continuously launch new business, CCW estimates that IT spending on new business-related solutions in the securities sub-segment will increase considerably in future.

For insurance companies, the overall IT infrastructure is still very nascent. Large players will invest more money into the development and update of core systems.

So we’ve just come out of the October holiday here in China and are headed in the final frantic few months before Chinese New Year. The difference this year is the early November once in a decade leadership transition where nearly every Chinese leader and politician will be replaced and/or shifted around in China’s Communist Party. It was never in doubt that the transition would happen towards the end of this year, but it was only in the last few weeks that it became clear it would happen in early November.

This is an important transition for the government and only the second peaceful transition of power in recent China’s recent history. The transition is even more important because of the critical social and economic challenges that the country is facing right now. A slow/stagnant world economy and increased but still limited domestic consumption is limiting China’s economy as a whole which is exacerbating the internal challenges it is facing – one of the most critical being the increasing delta between the haves and have nots. If you have been reading international media recently, we’re starting to see more and more of this discrepancy being uncovered and it does nothing to help the government in the eyes of the people.

More specifically to the financial industry however, the transition means increased change. We’ve seen this already this year especially in the capital markets as the new chief regulators have done quite a bit to open the capital markets this year with increased rumours that regulation on the RFQLP programme should be announced shortly, adding yet another channel for off-shore RMB to come back into China’s mainland markets.

The shift in policy is also indicative of China’s increased awareness of money leaving China. With reports of both wealthy individuals and corporations legally and illegally sending money abroad, the issue which used to be too much hot money coming in, is now too much hot money going out. To a certain extent, this is a bit of a blessing in disguise for China as it will allow regulators to further open the market without risking the hot money inflows – which was viewed as a challenge in the past.

With the party congress set for November of this year, we’re unlikely to see too much more change until after Chinese New Year (Feb 2013). What we should be able to quickly determine though is how open the new leaders are to change and modernization of all industries, not just the financial services industry. As we’ve discussed on our blog before, this will largely depend on how quickly the new leaders can consolidate their power to be able to effect change and in which direction they decide to go.

Regardless, 2013 will be a new watershed for China’s financial services industry. Stay tuned early next year for our 2013 top financial technology trends report to see how we see things changing.

Mobile Banking in China continues to grow

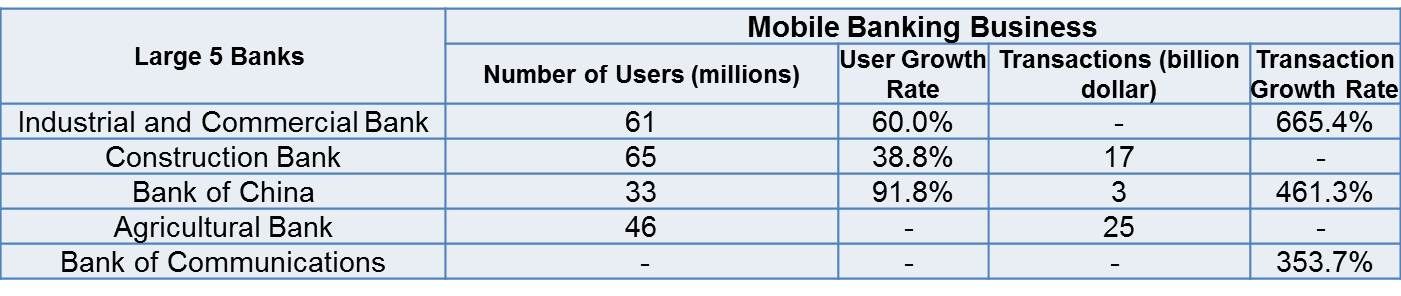

According to the latest semiannual reports issued by China’s commercial banks, e-banking continues to grow in importance as a part of banks’ business. For most of banks, e-banking channels has already contributed to over 60% of total transaction volume with the 5 large commercial banks’ total e-banking transactions showing a 35% growth rate year on year. Benefiting from the advancement of IT and the proliferation of smart mobile phone in China, mobile banking has become increasingly convenient for users and important for banks.

In order to meet the strong demand for mobile banking, banks continue to update their mobile banking applications and launch new functions to enhance the user experience. For instance, Agricultural Bank released its new iPhone-enabled mobile banking app which not only supports banking transactions but also integrates online shopping. Bank of China launched the first Windows-enabled mobile banking application recently. We expect that in the future banks will offer more value-added services on their mobile banking products through innovations and ensure safe and reliable systems.

China’s banking IT spend will continue to grow strongly

In 2013, China will take over Japan as the biggest consumer of IT products in Asia. According to IDC, China's total IT market size in 2012 is projected to reach 155 billion US dollars, with 20% growth rate YOY, and in 2013, this number will reach 170 billion dollars, 4% more than that of Japan. During China's Five Year Plan period (from 2011 to 2015), companies must invest more in their IT infrastructure to meet the demands of stable growth and innovations.

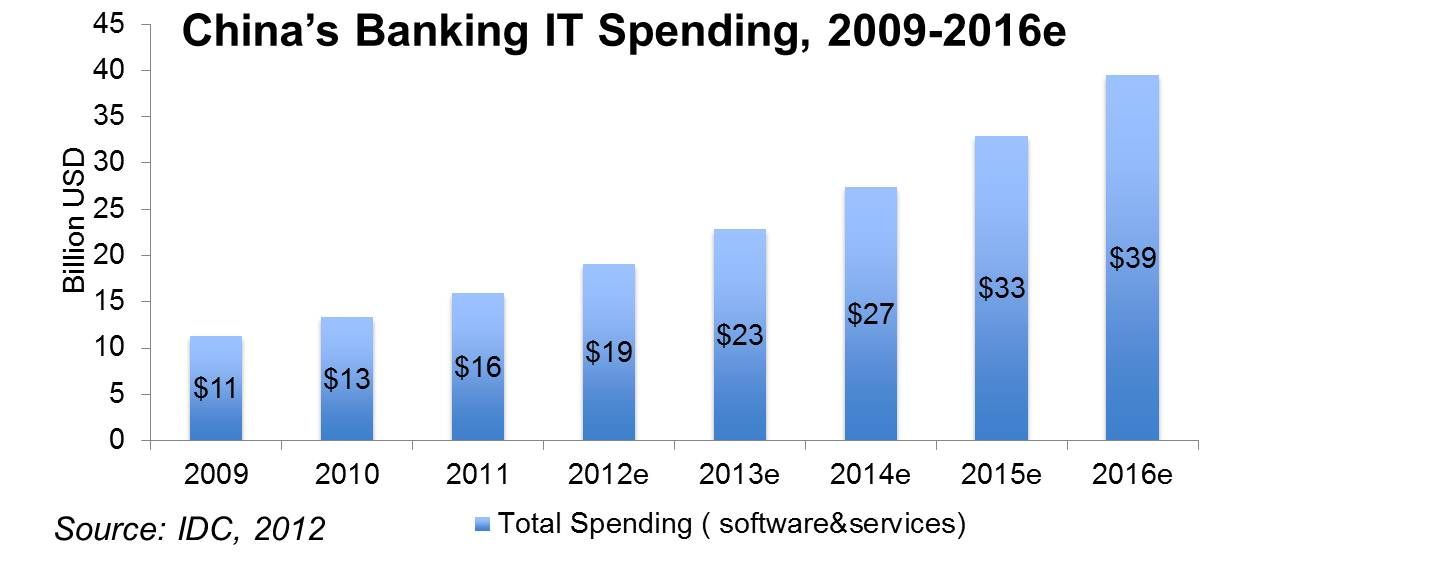

In the banking industry, total IT spending (software and services) in 2011 exceeded 15 billion US dollars, with a 19% growth rate compared to 2010, and, according to IDC, China's banking IT spending will keep a 20% CAGR (Compound Average Growth Rate), hitting 39 billion dollars in 2016. We expect that the new generation of core banking systems, risk control, big data analysis and mobile payment will be the main driving forces behind the IT spend.

Banking on China, a Kapronasia and Oracle report looking at challenges for international banks in China now available

The Banking on China report is now available on the Kapronasia website in the research reports section. The report from Oracle and Kapronasia looks at the key challenges and opportunities for international banks in China and is based on numerous interviews with both larger and smaller banks in China. The complimentary report is available for download after you have logged into your Kapronasia.com user account. If you do not have an account, register today for free.

Reform in China’s Banking Sector: More to come?

In recent years, Chinese banking sector profits have skyrocketed to new levels, in part due to the Beijing imposed ceiling on the rates banks pay depositors, providing banks with a source of cheap funds, which banks then in turn lend out at much higher rates. Net profits for commercial banks grew 36 percent last year, reaching 1 trillion Renminbi. Chinese banks are enjoying year-on-year rises of more than 30 percent in their first-half net profits. In one example, the Industrial and Commercial Bank of China’s fees and commission income for the year 2011 was close to 100 billion RMB, compared to 72 billion in 2010 and 55 billion in 2009.

The Technical Challenges for QDII funds in 2012

Since the first QDII quota of US$500 million was allocated to the HuaAn fund in 2006, the quota allocated to security companies and fund companies has maintained steady growth. As of the end of February 2012, US$44.4 billion of investment quota was allocated to fund companies and security companies, compared to US$44.4 billion and US$40.6 billion for 2011 and 2010.

More...

Disaster recovery systems for China’s banks

In recent years, since Chinese banks have been working on data consolidation at the national level, the establishment of disaster recovery systems has become one of the key considerations for banks. Today, banks must ensure the stability and security of their national data center in the event of a disaster to ensure uninterrupted business operation through disaster recovery systems.

According to IDC’s report “China Business Continuity and Disaster Recovery Market Forecast, 2008-2013, data disaster recovery service and business continuity in China is expected to become the fastest growing segment in the local IT service market during 2008-2013, with a CAGR of 52%.

A standard recovery

The importance of disaster recovery systems has pushed the Chinese government to formulate a series of industry standards. In June 2009, the China Banking Regulatory Commission issued a new guideline on IT Risk Management of Commercial Banks, which has set a higher standard for the information security and business continuity of the entire life cycle of banking IT.

In 2011, China’s regulators also urged local banks to speed up the implementation of disaster recovery systems during the 12th Five-Year Period, by proposing a disaster recovery model named “Two Places and Three Centers”, which specifies a main data center, a remote disaster recovery center, and an intra-city emergency disaster recovery center.

In response to the legislation, recently, more local banks have started building their own “Two Places and Three Centers”. Large domestic banks have been seen allocating more resources to develop the disaster recovery model and already built large disaster recovery centers. The Agricultural Bank of China initiated its Shanghai remote disaster recovery center in 2012; China Construction Bank will complete the establishment of its Beijing data center in 2013. Even though they are somewhat behind the larger banks, small and medium banks have identified “Two Places and Three Centers” as one of their key IT investment priorities in the future.

Looking forward

In 2012, we expect that local small and medium sized banks will lead the demand for disaster recovery systems, particularly for joint stock commercial banks and city commercial banks, as they seek national expansions in their next phase of growth. With increased operating risks, banks have begun to put more value on the benefits brought by disaster recovery systems, which will be key to ensure uninterrupted business operation and improve risk management capability. This trend is also likely to be seen in local insurance and securities sector, where more small and medium sized insurers, securities firms and fund companies will invest in disaster recovery systems.

Compared to self-built disaster recovery centers, outsourcing services on disaster recovery will be much more popular among these companies, as the latter can provide lower investments, shorter construction period and higher service standards; the local market for disaster recovery system is still dominated by global players represented by IBM, HP, Symantec and EMC.

China's disparate Financial Standards

As China’s financial institutions continue to invest more money in information technology innovation to help them maintain strong growth and a competitive edge, foreign vendors expect enormous opportunities and are scrambling to enter this dynamic market.

However, when a foreign vendor and its local partner want to implement a new solution, both of them may face a dilemma or, specifically speaking, a real problem, in that China’s financial standardization lags behind the relatively rapid development of the financial industry globally and has yet to meet the demands of technology innovation and business expansion. This can slow the pace of technology advancement as competing standards add layers of complexity and make it more difficult to come up with straightforward technology solutions to clients’ problems. The PBOC has realized that financial standardization does and will continue to play a pivotal role in financial informationization and regards standardization work as an important strategic measure to promote China’s financial industry.

The China Finance Standardization Technical Committee (CFSTC), established by the PBOC and other financial institutions, shoulders the responsibility to draft and revise financial standards relating to banking, insurance, security and printing, and it also promotes the adoption of new standards in China. As of the end of 2011, CFSTC had issued 151 financial standards covering fundamental data elements, code, interface standards, terminology, messages, data, financial instrument designs, and parameters in printing technology. These standards have been successfully implemented in various financial areas such as bankcard, Internet Banking, accounting, treasury, information security and financial IC card.

Take for example the ISO 20022 standard, a universal financial industry message format. Since China has become a member of WTO, the scope of China’s financial institutions’ business has become much more international than before. However, incompatible financial message formats increase the cost of international transactions and impede efficient global bank connectivity, so the PBOC has already urged China’s local banks to adopt the ISO 20022 financial message standard and, at the end of 2011, CFSTC also issued the ISO 20022 standards which will be officially implemented in May, 2012.

We can expect that local banks will obtain numerous benefits from the implementation of ISO 20022 in China including the reduction of transaction costs and improvement of risk control. Vendors, of course, will be happy to help banks upgrade their cash management, treasury and payment systems.

Although progress has been made, China’s financial standardardization still faces many problems and challenges:

- Compared with the large number of services offered by China’s financial institutions including banks, security companies, and insurance companies, the number of standards is not enough and the variety of standards is limited. For example, even though electronic payment business, such as online banking and mobile payment is increasingly popular in China, China still lacks sound and comprehensive electronic payment standards which will standardize the end-to-end process of electronic payment and control payment risk.

- 70-80% of total standards refer to information technology, and CFSTC needs to draft more standards related to business and management, such as operation, transaction and risk management standards

- Experts with relevant industry experience and knowledge are scarce, hindering the draft of standards

- Currently, China only follows international standards, instead of participating the drafting of international standards

As China becomes further integrated into global financial markets and reformation of domestic financial markets continues during the 12th Five-Year Plan Period, the authorities realize that they should continue pushing financial standardization and, more importantly, participating more actively in the drafting of international standards. By submitting its own proposals for international financial standards, China wants to strengthen its competitive edge in global financial markets.

Although it seems difficult for China to exert influence on international financial standards over the relatively short period of time that China’s markets have been developing, CFSTC will keep tracking and learning international standards first and promote indigenous innovation at the same time. In the future, we will likely see some of China’s own financial standards become international standards.

A sizeable portion of Chinese customers are willing to try new methods that may offer them increased convenience over the current need to go to the branch for any problems. Due to the sluggish pace of personal banking in China, consumers have shown added interest in electronic services that will shorten the time they spend in any bank branch. Chinese consumers have also expressed interest in using the internet more in finding out about new products and services as well as using the internet more in addressing account problems.

Among the report’s insights, was the finding that in both the United States and China, a low level of trust in system security remains a considerable obstacle for the integration of social media in banking. Although Chinese consumers seem to be slightly less sceptical than their American counterparts, both groups are unconvinced that social media is a safe route through which banking transactions can be conducted. Although if consumer confidence can be instilled in the safety as well as the privacy factors in social media, both groups would welcome a more technologically advanced system since they believe social media can make their banking experience more expedient and convenient.

With hundreds of millions of individuals in both China and the United States partaking in social media activity each and every day, possibilities of combining social media with other aspects of life are constantly being discovered and experimented with. The key to a successful implementation is the correct assessment of the public’s level of readiness before taking swift action to modernize.

Kapronasia’s latest report “Social Media and Banking in China” takes a comprehensive look at how social media will change the personal banking landscape in China as well as the attitude both American and Chinese consumers hold toward the use of social media in the future. This report, the first of its kind in examining the realm of social media and banking in China, lends many key insights critical to understanding the thoughts and actions of Chinese consumers. These and other findings will be discussed in detail during a Kapronasia webinar on the Social Media and Banking in China” report in early April.

Prepaid card recycling in China

One of the most interesting parts of doing market research in China is learning about the innovative ways of doing business. A few weekends ago the fracas over the China launch of the iPhone 4S at the Apple store in Beijing got me thinking. If you haven’t followed the story, basically, the store was meant to open in the morning and people had queued all night for a chance to buy one of the new phones. The store eventually never opened that day with Apple citing staff safety concerns much to the ire of the people who had braved the cold.

If you look at pictures and reports of the event, it’s clear that many of the people who were queuing and waiting were not necessarily the typical iPhone user. Many of them are in fact what are called huangnius (yellow cows) who are the scalpers who buy the iPhone 4S at retail for about US$790 (as compared to US$650 in the US for a 4S 16GB unlocked) and then sell it on the gray market for a 20%+ markup.

Huangnius are not just limited to electronics though. Actually the first that I had heard about them was when I arrived to shanghai a number of years ago and wanted to exchange RMB for USD. You can go through the banks, but as the currency is capital controlled, you are limited to how much you can convert. No limits to the amount of RMB the huangniu will buy though, of course you’ll have to take his rates, but if you need the USD, you need the USD. The award for best business model though, has to go to the huangniu that are involved in the pre-paid card industry.

As we discussed in previous commentaries, pre-paid cards in China are very popular and are often given by companies as part of an annual bonus to their employees. A key part of that equation are the ‘fapiao’ or official invoices that they receive for the cards. In order to account costs in China, you need to have an official fapiao that is submitted to the tax authorities to show that you actually did incur an expense and aren’t just faking invoices. There are of course ways that companies counterfeit fapiao or buy actual fapiao, but that is a whole separate subject.

Back to the prepaid cards and the huangniu, so in the west, there are of course a number of companies that will give you money today for your money tomorrow. Similarly, the huangniu openly purchase pre-paid cards. So let’s go through how this whole process works:

A large company, let’s call it ACME, will purchase a number of prepaid cards from a prepaid card issuer such as a large retail store chain for typically what is the actual face value of the card, let’s say 1000 rmb (renminbi or rmb for short is another name for Chinese Yuan; 1000rmb is about US$150). ACME will pay the issuer and receive the official receipts (fa piao) from the issuer and be able to claim either as a business or salary expense depending on ACME’s accounting and then will give the cards to their employees as part of their annual bonus or just as part of their regular compensation.

Now, say the prepaid card is only good at the issuer’s store and the ACME employee who received the card rarely shops at that store, or just really needs the money right away. They can then contact a huangniu who, if it is a popular kind of prepaid card, will buy it off the ACME employee for a certain percentage of the original value, let’s say 800 rmb in this case. The huangniu at that point has a number of options including reselling it to an individual consumer who might be interested in the card for say 900rmb, thus making a 100rmb profit. This makes a lot of sense, and when it was explained to me, wasn’t surprising.

What was surprising to me in this case is that the huangniu will sometimes sell it back to the issuer themselves. So think about this, the issuer has sold the card for 1000 rmb and immediately that becomes a liability for the company (similar to a loan for a bank) as the user can then use that card to purchase goods. Not trying to make things overly simple here, but what the issuer would love is that the users never in fact use the cards and they expire along with their complete value. That 1000rmb suddenly moves from being a liability to a cash asset. If that isn’t possible, the issuer would want to get the most value back from the card as possible.

So to do that, the issuer will actually buy the unused card from the huangniu at a slight discount. So in this case, say it was 900rmb. So the issuer has cleared off 1000rmb of liabilities for 900rmb and everyone in the ‘value chain’ is happy. The issuer is happy as they make a tidy profit and are then able to reissue the card at the same 1000rmb value which accelerates the ‘velocity’ of the card in the market so that it appears more popular. ACME is happy because they have compensated their employees and have received official receipts which they can then deduct from their tax bill. Employees are happy because they have 800rmb in cash. Huangniu are happy because typically the sellers are buyers of these cards are fixed which means steady regular and predictable profits.

The values used here are just examples. From others in the industry it seems that these arrangements happen for as little as a 1rmb discount on each card. So the huangniu will buy the card for 99rmb instead of 100rmb and then sell it for 99.5 rmb or similar. Even with such a small discount, they still manage to make huge profits through volume.

The key takeaway from all of this is that China is developing rapidly and many of the regulations in and around the finanancial services industry are somewhat vague and often allow for loopholes similar to the model I laid out above. These inevitably will be sorted out in the future, but for now, it is another example of the inventiveness of the market players and the lack of specific regulations preventing what is essentially a huge tax dodge and license to print money.