China Banking Research

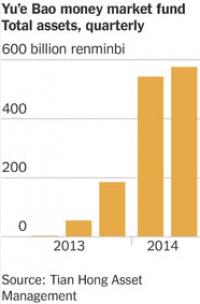

With the Alibaba IPO behind us, what about Yue bao's future?

In the wake of the largest IPO in the U.S., there has been increased attention on China's innovation and its potential disruptive nature on global banking and e-commerce. Yue bao's future strategy is in the spotlight once again.

What does tokenization mean for China?

Tokenization seems have become a buzzword since the Apple Pay announcement. However, the technology itself is not new.

China's online banking and mobile banking continue to drive ahead

China's online banking and mobile banking continue to be the key channels for customers who interact with their banks through 'e-channels' as data from iResearch, a Chinese online customer survey service provider, shows.

Chinese P2P Lending growth coming from Five Most Developed Regions

According to Online Lending House, an internet finance news source, P2P transaction volume has reached RMB 81.84 Billion in 1H2014. The most active regions are Guangdong, Zhejiang, Shanghai, Beijing and Jiangsu.

On July 25th, Shang Fulin, the chairman of CBRC, disclosed three private banks that had been approved by the CBRC. Hua Rui Bank, planned to be set up by Fosun and Juneyao, was not on the list. Later the Shanghai branch of CBRC revealed that the Fosun and Juneyao partnership had broken up.

Kapronasia's new report entitle "China Moving Abroad - A look at the legal...and not so legal ways Chinese nationals are moving their money abroad" is now available for download on Kapronasia.com. To view and download the report, please go to our research section here.

Direct Banking model Favored by City Commercial Banks

Earlier this year, we published our 2014 “Top-10 China Banking Industry Trends” report and predicted the advent of direct banks. We were right: in a month Minsheng Bank rolls out its Chinese direct banking institution.

Alibaba Teams up with Banks to Launch Unsecured Loans

On July 22nd, 2014, Alibaba teamed up with seven banks including ICBC, CCB, CMB, Ping An Bank, Postal Savings Bank of China, Bank of Shanghai and Industrial Bank to roll out new internet business loan service.

Will VTMs disrupt the ATM industry in China?

China has been going through rapid urbanization during last decades and in the past ten years alone the percentage of population residing in cities has leapt from 40.5% in 2003 to 53.75% in 2013.

The “Notice on Government-set Prices and Government-Guided Prices for Commercial Banking Services”, published by National Development and Reform Commission (NDRC) and China Banking Regulatory Commission (CBRC), is effective on August 1st, 2014.

More...

China is beginning to open its financial sector with the approval of three privately owned banks, extending the wave of financial reforms aimed at boosting China's changing economy.

Talks China – US - July 2014

Earlier this month, the US and China held their annual talks in Beijing, where they discussed trade, economic, regional, and political concerns.

Kapronasia's ATMs in China 2014 webinar and slides are now available in the webinar section of the website or by clicking here.

Currently there are 637 companies on the IPO list in China and their prospectuses, published by the China Securities Regulatory Commission, reveal business intelligence, previously not available for public.